Energy news - April 2026

A roundup of the latest energy news in April 2026, including market update on Electric Vehicle (EV) charging infrastructure, results of the AR7a for solar and wind projects, recent energy headlines, as well as upcoming events.

EV charging market update and ESPO framework success

The UK’s EV charging network has consistently grown over the past few years, creating both opportunity and complexity for local authorities, public bodies and landowners. Public charging devices have increased from fewer than 30,000 in 2021 to over 116,000 by the end of 2025. Importantly, growth is happening across both urban and rural areas, reflecting a more mature and accessible network as EV adoption accelerates nationally.

A major trend shaping land and property strategy has been the rapid rise of high-power charging. While lower power destination chargers still play a vital role in residential properties, workplaces and leisure locations, the strongest infrastructure growth is in rapid (50-150kW) and ultrarapid chargers (150kW and above). More than 3,400 rapid charge points were added to the public network in 2025 alone. These chargers are key for strategic locations such as retail parks, key transport routes and high traffic public assets. For landowners, creating an EV hub can generate meaningful revenue, increase footfall and help deliver local net zero goals.

The UK’s EV model range has also expanded significantly, with more than 130 fully electric vehicles now available, covering every major vehicle type from small city cars to long-range SUVs and vans. Affordability is improving as battery costs fall and competition grows, while the Zero Emission Vehicle (ZEV) mandate continues to push manufacturers to increase EV supply. With more than 1.75 million EVs already on UK roads, we expect that public charging demand will continue increasing across all regions.

Commercial fleet electrification adds another dimension. Electric vans now represent more than 8% of new registrations, and zero emission buses account for more than one in four new vehicles entering service. Electric HGVs are beginning to scale, driven by new vehicle availability and operators trialling high power depot and hub charging setups. Over time, we expect that this transition will require more sites with higher grid capacity, which will likely require a grid-led strategy.

Commercial models

For local authorities, other public bodies and landowners, understanding commercial models is key to unlocking the opportunities available:

Rental model

In the rental model, the charge point operator (CPO) pays the landowner a fixed annual site rent, often on a per charger basis, for the right to install and operate the chargers. This is ideal for those seeking stable income with minimal involvement.

Benefits:

Guaranteed, predictable income;

Minimal risk or operational responsibility for the landowner; and

Simple commercial arrangement.

Revenue share model

This is a revenue model for public or semi-public sites and is sometimes offered as a ‘higher of’ option for either rental or revenue share. The CPO funds the installation, operation and maintenance, while the landowner receives a share of the revenue generated. This is typically calculated as a percentage of gross annual profit. This is ideal for busy sites, retail environments, car parks, destinations with strong footfall and ultimately the potential for high-charger utilisation.

Benefits:

No capital expenditure for the landowner;

Shared upside as charging utilisation grows; and

Operator is incentivised to maximise performance.

ESPO Framework

As an approved supplier on the ESPO Framework, Lot 4 (EV Charging Consultancy), we provide a procurement ready route for public bodies such as local authorities. Our services include feasibility studies, commercial, operator procurement, planning and grid engagement, business case development, and end-to-end project management.

Through ESPO, any public body can access expert support from Carter Jonas quickly and compliantly, ensuring your EV strategy is commercially sound, futureproofed and aligned with local NetZero ambitions.

Please reach out to Jamie Baxter (Jamie.Baxter@carterjonas.co.uk, 07598580511) for more information.

Record results for solar and onshore wind in CfD Allocation Round 7a

AR7a delivered a record 6.2GW across the onshore technologies, consisting of 4.9GW of solar, 1.3GW of onshore wind. Together, these results build on the separate offshore wind auction which was announced earlier in the round, and helps to provide route-to-market certainty for a range of projects.

The 4.9GW of solar capacity securing 20-year CfDs is particularly strong. The strike price for solar was set at £65/MWh in 2024 prices, which is a 6.5% reduction compared to the previous strike price from AR6. This outcome signals heightened investor confidence and reinforces the expanding role of utility-scale solar in the national energy mix.

Onshore wind also performed strongly, with 1.3GW securing contracts at a strike price of £72/MWh, which is a 2% increase compared to AR6. To provide some context, the average wholesale price for the UK for 2025 was upwards of £80/MWh, and the cost for new-build gas stations to operate is estimated to be around £147/MWh. On that basis, onshore wind remains highly cost-competitive, and the volume secured points to a healthy pipeline of viable projects progressing.

At a time when energy security is even more in focus, these renewables projects will deliver critical national infrastructure, shoring up the resilience and stability in the energy market in the medium term.

Recent headlines – Grid connection delays, substation bay sharing, and questions around connections reform

Renewables projects with 26/27 connection dates hit by delays

Transmission Operators have delayed the connection dates of 210 projects due for connection in 2026/27, which represents 62% of protected projects. This has prompted Ofgem to express its frustration and ask for clearer communication from NESO, alongside more ambitious delivery dates.

These delays underline the extent of congestion across the grid network. As schedules continue to slip, we are seeing developers revisiting commissioning plans, financing arrangements, and deployment assumptions.

These timing issues between project development and grid offers is creating a challenging environment for developers, compressing decision windows and increasing delivery risk at a time when confidence in grid is essential for market momentum.

Substation bay sharing being considered by DESNZ and Ofgem

Transmission Operators are reporting high levels of oversubscription among solar and battery projects relative to CP30 requirements. In response, DESNZ and Ofgem are considering mandatory bay sharing to make better use of existing substation capacity.

While this could unlock additional capacity and speed up access to the grid, it also brings challenges. Bay sharing may weaken traditional connection rights, increase curtailment risk, and introduce more complex legal and operational arrangements between collocated schemes. This represents a notable shift in how developers may need to structure commercial agreements and manage asset risk, especially in areas where competition for capacity is intensifying.

Uncertainty around queue management and future gate processes

Key parts of the new connections reform process are still unclear. The date for the first ongoing application window has not been confirmed, and there is no detail yet on how projects leaving the queue will be replaced by those in Gate 1.

There is also uncertainty over how <5MW schemes will be handled under the forthcoming Local Power Plan. This lack of clarity continues to complicate planning for developers of all sizes, making it harder to forecast queue movements, progress land agreements, and align project timelines with grid capacity.

Energy Market Update

In a volatile and developing market, Carter Jonas’ Procurement Platform helps clients to find the best PPA price for their export generation as well as options for sleeved PPAs and gas and electric supply contracts. See below for this week's latest on the UK & EU gas, UK power & renewables and the oil & carbon markets, in partnership with PPAYA.

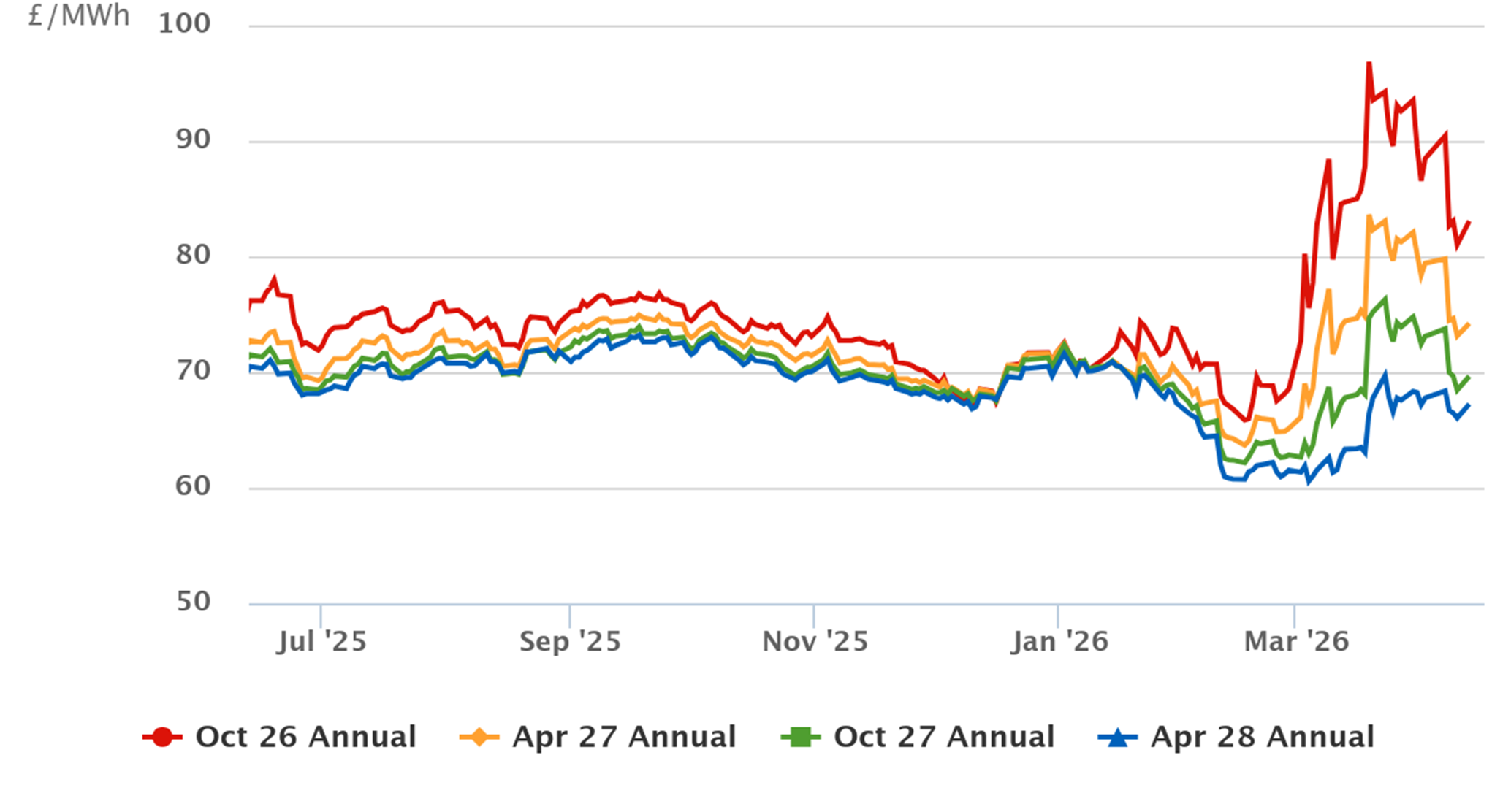

Annual Forward Power Curves for April 2026

Weather

Temperatures across the UK are expected to trend cooler through the remainder of this week and into early next week, before gradually returning to seasonal norms from the start of April.

Gas

During yesterday’s session, prompt gas contracts fell by around 5% following reports of productive conversations towards a potential resolution in the Middle East. However, this morning Iran pushed back on the narrative, stating that the Trump administration was “negotiating with itself”.

Overnight, Iranian missile strikes continued across Iraq, Kuwait, and Saudi Arabia, including hits on a fuel depot at Kuwait International Airport and an army medical centre in Iraq’s western Anbar Province.

Despite ongoing military activity, prices have edged lower again this morning, suggesting the market is being driven more by sentiment around a potential resolution than by any confirmed de-escalation.

Norwegian flows remain robust, with Gassco reporting total nominations of 322.6 mcm/d, including 53.4 mcm/d to the UK. Overall capacity remains constrained due to planned maintenance at Aasta Hansteen.

According to AGSI+ data, pan-European storage stands at 28.42%, while UK reserves are at 36.12% capacity.

Power & renewables

Total UK demand is currently 38.8GW, with domestic generation supplying 37.4GW and imports from neighbouring markets accounting for the remaining 1.4 GW.

Solar generation remains robust at 7GW, benefiting from the recent spell of sunnier conditions across the UK. Wind output is exceptionally strong this morning, contributing 23.2GW, around 60% of total domestic output.

Nuclear capacity is gradually recovering as reactors return to service across the fleet, including the full return of Hartlepool, bringing total nuclear baseload to 4.46 GW this morning.

Oil & carbon

Brent Crude prices fell sharply on Wednesday 25th March, slipping below the $100/bbl mark as sentiment turned heavily bearish on expectations of a potential ceasefire in the Middle East, despite Iran maintaining that no such discussions have taken place.

Upcoming events

Our Energy & Consents team (Charles Hardcastle, Stuart Campbell, Simon Tarr, Helen Moffat, Tom Allen, Philippe Rottner, Kate Girling, Georgie Spens and Alex Ireton) will be attending All Energy in Glasgow this May 13-14.

Our Consents and Natural Capital team (David Walker, Kate Girling, Willow Mercer, Nanayaa Ampoma, Georgie Spens, Lucy George, David Alborough, Sophie Davidson) will be attending and hosting UKREiiF fringe events this May (19-21) in and around Leeds.

Philippe Rottner will be attending Solar & Storage Live this April (29-20) at the Excel, London.

Please get in touch if you would like to meet up with anyone in the team.